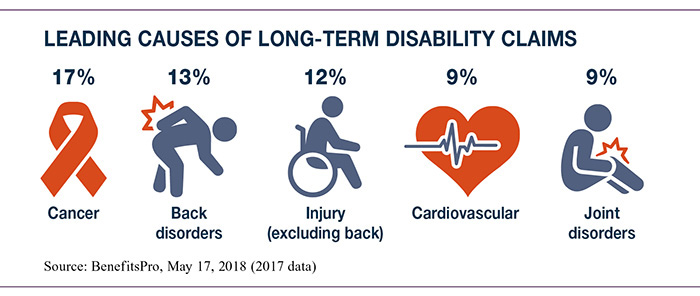

09 Jan Consider a Customized Disability Insurance Policy

If you are in good health, disability insurance may not be high on your list of financial priorities. But the statistics might surprise you. A 50-year-old has a 36% chance of experiencing at least one disability lasting 90 days or more before reaching age 65.1

Less surprising, perhaps, is that older people often take longer to recover from a serious disability. A 55-year-old who experiences a 90-day disability has a 60% chance of it lasting for at least five years.2

Even if you have a solid emergency fund, an extended period away from work could strain your family finances and alter your options for retirement.

Portable Individual Coverage

If you’re concerned about the potential effect of losing your paycheck due to sickness or injury, you might consider an individual disability insurance policy. Your employer may offer long-term disability coverage, but group plans typically don’t replace as large a percentage of income as an individual plan could, and benefits from employer-paid plans are taxable to the employee if the employer paid the premiums. Of course, if you change jobs, you might lose your subsidized employer-based coverage.

An individual disability income policy could help replace a percentage of your income, up to the policy limits, if you’re unable to work due to illness or injury. Benefits may be paid for a specified number of years or until you reach retirement age. If you pay the premiums yourself with after-tax dollars, benefits are usually free of income tax.

Customizing Disability Insurance Coverage

Unlike group policies, an individual policy can generally be customized to meet your specific needs. Here are some common riders. All benefits are up to the policy limits.

Residual benefit — May help replace lost earnings after you return to work part-time or at a lower-paying job.

Own occupation — Determines a disability by your inability to perform the duties of your specific occupation or profession, as opposed to being unable to work in any occupation.

Automatic benefit enhancement — Provides an annual benefit increase each year for a period of years to help keep up with increased earnings. Your premium will also increase.

Future increase option — Allows you to increase benefits (for a higher premium) without medical underwriting.

Cost-of-living adjustment — Adjusts the amount of monthly disability benefits each year during the disability.

Disability premiums are based on your age, gender, occupation, and the amount of potential lost income you are trying to protect, as well as the specifics of the policy and any additional benefits that are added.

1, 2 2018 Field Guide, National Underwriter

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc.