May 08, 2019 Bonds Can Offer Stability Even with Rising Rates

Bonds can be a tricky investment when interest rates are rising, as they have been for the last few years. The value of bonds sold on the secondary market typically falls as rates rise, because investors can buy new bonds with higher yields. (The reverse is true when rates are falling.)

Even so, bonds can play a pivotal role in portfolios as a source of income and to balance more volatile stocks in an asset allocation strategy. One way to address concerns with rising rates is to hold individual bonds to maturity. In this case, you would receive the principal and interest regardless of changing interest rates, as long as the bond issuer does not default. And with increasing interest rates, many individual bonds are offering higher yields, whether purchased new or on the secondary market.

Bond maturities typically range from 30 days to 30 years. Bonds with longer maturities generally pay higher interest rates but are more sensitive to changing rates. In the current environment, it may be more appropriate to focus on short-term and intermediate-term bonds, so you are in a position to take advantage of higher yields when your current bond holdings expire.

Types of Bonds

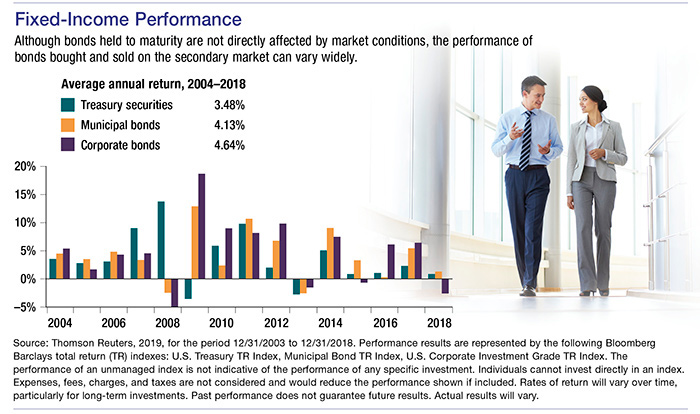

Bond issuers typically fall into three categories: U.S. Treasury securities, municipal bonds, and corporate bonds.

U.S. Treasury securities (bonds, bills, and notes) are generally considered among the safest investments because they are guaranteed by the federal government as to the timely payment of principal and interest.

Municipal bonds (munis) are issued by state and local governments. The rates paid by munis may be higher than Treasury securities but lower than corporate bonds with comparable maturities. However, the interest on bonds issued by your own state or local government is typically free of federal income tax. The compensation of tax benefits for lower yields tends to be more valuable for investors in higher tax brackets.

Corporate bonds may offer higher interest rates than Treasuries and municipal bonds with comparable maturities, but they are associated with a higher degree of risk, which varies based on the creditworthiness of the companies that offer them.

Discounts and Premiums

Corporate and municipal bonds are often sold with a face value of $1,000 and a minimum purchase of $5,000. Bonds purchased at less than face value are said to be purchased at a discount, and thus will offer a higher yield than the coupon rate (the interest rate stated on the bond). For example, if a $1,000 bond has a coupon rate of 4%, it promises to pay $40 annually, typically with half of the annual interest paid every six months. However, if the bond is purchased at a discount for $800, the annual yield is 5% ($40 ÷ $800 = .05 or 5%). A similar calculation applies when a bond is purchased at a premium for more than face value.

The principal value of bonds may fluctuate with market conditions. Bonds redeemed prior to maturity may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk.

Investors who buy a municipal bond issued by another state usually have to pay income taxes. Although some municipal bonds may not be subject to ordinary income taxes, they may be subject to federal or state alternative minimum taxes. If a tax-exempt bond is sold for a profit, investors could incur capital gains taxes.

Asset allocation and diversification are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc.