Feb 05, 2019 Need to Tap Your 401(k)? Proceed with Care

Everyone faces challenges, and some challenges require more cash than you have readily available. If you find yourself in that position, you might eye your 401(k) balance and consider using those funds to meet your present needs. That’s a natural response, but it’s usually not a good idea.

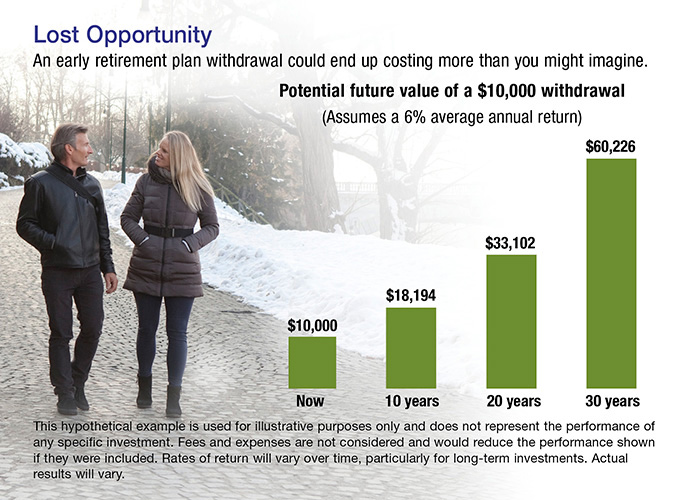

Taxes and Lost Growth

If you are younger than age 59½, you generally cannot withdraw funds from your employer’s retirement plan while you are still employed, unless you qualify for a hardship distribution (explained later). If you are older than 59½, some plans may allow an in-service distribution. Even if you are eligible, all distributions from a traditional 401(k) are subject to ordinary income tax, and a 10% federal income tax penalty generally applies to withdrawals before age 59½. If you are in the 22% federal income tax bracket, a $10,000 withdrawal might put less than $6,800 in your pocket ($10,000 minus $1,000 penalty, $2,200 federal income tax, and any state income tax).

That’s a significant deterrent in itself, but the greater penalty could be the loss of future savings growth needed for retirement (see chart).

Consider a Loan Instead of Your 401(K)

If you really need to tap your 401(k) funds, a loan might be a better option, as long as loans are allowed by your plan and you anticipate staying with your employer long enough to pay the loan back. Under IRS rules, loans are limited to the lesser of $50,000 or 50% of the vested account balance. Loans must be repaid within five years (longer terms may be allowed for a home purchase). However, each plan is allowed to set its own interest rates and repayment policies. The good news is that even though the plan is required to charge interest, the interest is paid back to your own account.

Of course, borrowed money isn’t pursuing investment returns, so your retirement savings goals may be interrupted as long as the loan is outstanding. If you leave your employer, you have until October of the following year (the federal income tax extension deadline) to put the borrowed money back into the old plan, a new employer plan, or an IRA. Failing to repay on time means the outstanding balance may be treated as a distribution and subject to ordinary income tax and the 10% early-withdrawal penalty.

Hardship Distributions

Although not required to do so, a plan may allow participants to take hardship distributions limited to the amount necessary to meet an “immediate and heavy financial need.” Before taking a hardship distribution, you must take advantage of all other available distributions, including loans. The employer can make its own determination as to hardship, but the IRS considers the following situations to meet the definition:

- Medical expenses for the employee, the employee’s spouse, dependents, or beneficiary

- Costs directly related to the purchase of an employee’s principal residence (excluding mortgage payments)

- Tuition, related educational fees, and room and board expenses for the next 12 months of post-secondary education for the employee or the employee’s spouse, children, dependents, or beneficiary

- Payments necessary to prevent the eviction of the employee from the employee’s principal residence or foreclosure on the mortgage on that residence

- Funeral expenses for the employee, the employee’s spouse, children, dependents, or beneficiary

- Certain expenses to repair damage to the employee’s principal residence

Keep in mind that, as with other withdrawals, a hardship distribution is subject to ordinary income tax and a potential early-withdrawal penalty.

This information is not intended as tax, legal, investment, or retirement advice or recommendations, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Broadridge Advisor Solutions. © 2019 Broadridge Investor Communication Solutions, Inc.